Across Accounting Today’s “State of PE in Accounting 2025” survey, our recent webinar discussion, and conversations at the PE Summit, one pattern became increasingly clear: a performance divide is widening across the accounting profession. Some firms are accelerating into a new operating model. Others are maintaining structures and assumptions that no longer reflect market realities. The distance between these two paths is growing quickly and the next 24 months will be decisive.

Many firms underestimate their capital needs, but pressure is building

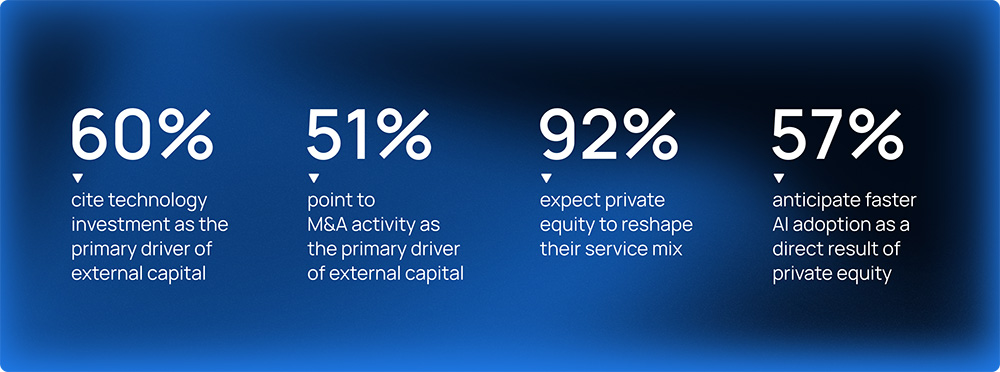

In the Accounting Today survey, most firms reported limited capital needs. Yet the drivers that require investment are growing stronger. Modernization, succession planning, talent constraints, and the shift toward higher value advisory work all demand resources.

Across the PE Summit discussions, firm leaders and private equity sponsors agreed that the real capital needs will materialize sooner than expected. These needs are tied to opportunity, not distress. The firms that want to improve margin, strengthen governance, modernize infrastructure, or build AI-enabled workflows will need structured investment to support those goals.

According to the Accounting Today survey, firms say the following is driving the need for external capital:

PE-backed firms are moving faster and increasing the performance gap

One recurring theme at the PE Summit was how quickly PE-backed firms are advancing. Their governance structures are aligned, their capital is designed to support modernization, and their decision-making processes are more coordinated.

These firms are modernizing data infrastructure, adopting AI earlier, integrating acquisitions efficiently, and scaling advisory practices with confidence. These actions create compounding advantage, which is already visible in the market.

AI is accelerating the separation

AI magnifies whatever foundation a firm already has. During our webinar with Accounting Today, we discussed how AI readiness is becoming a new indicator of firm competitiveness. The firms that benefit most from AI are not those experimenting with isolated use cases. They are the firms that have invested in governance, data foundations, and cloud-based systems that allow AI to be applied consistently across the practice.

Firms without these foundations cannot activate AI at the same pace. As more firms move forward, the speed and capacity advantage grows.

Why some firms face more pressure than others

This widening divide is not abstract. It reflects specific structural realities that influence how quickly a firm can respond to change. Based on the Accounting Today research and PE Summit discussions, the firms facing the most immediate pressure are those that:

- rely on aging systems that limit AI adoption

- have diffuse governance structures that slow decision-making

- lack capital or the ability to deploy it quickly

- face succession and demographic pressures that reduce reinvestment capacity

- cannot modernize at the speed of PE-backed competitors

These characteristics often appear in mid-sized and non-PE-backed firms, although size alone is not the determining factor. The underlying issue is the firm’s ability to align leadership, capital, and modernization to support a new operating model. Without that alignment, firms encounter delays that compound over time.

What leaders should focus on next

Across all of the conversations and data points, three strategic actions surfaced as the most important for firms preparing for the next phase of competition.

- Reassess capital needs and act proactively.

Modernization, AI adoption, and succession transitions are investment intensive and the timelines are shortening. - Create alignment at the leadership level.

Governance clarity ensures that modernization is strategic, not fragmented or incremental. - Treat AI as an embedded service-delivery capability, not a technical experiment.

AI will influence how firms deliver work, create value, and make decisions. It will not be optional.

The bottom line

A structural separation is emerging within the profession. Firms that can align governance, capital, and modernization will accelerate. Firms that pursue incremental change will fall behind, often gradually at first and then decisively.

The next 24 months will define that divide.

Download my whitepaper, Accounting at the inflection point, to dive deeper.